Sledujte nás pro

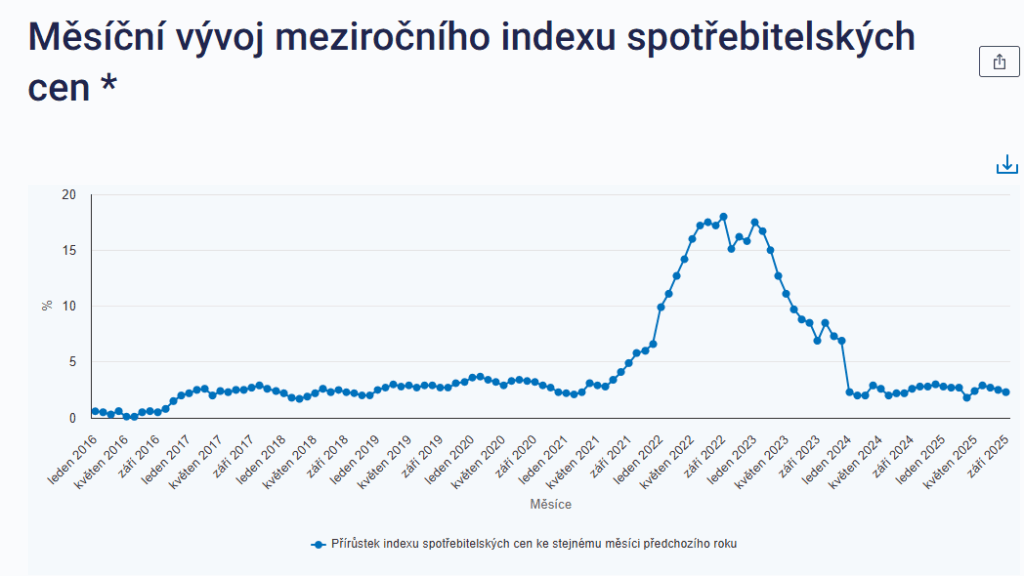

Sledujte nás proV pátek 10. října Český statistický úřad zveřejnil míru inflace za srpen 2025. Stejně jako ve všech předchozích měsících se skutečná hodnota shoduje s odhadem zveřejněným před několika dny.

- Meziroční míra inflace pokračuje v poklesu. Dosažených 2,3 % je nižší než srpnových 2,5 % a jedná se o nejnižší meziroční tempo od dubna. Zároveň je nižší než odhad ČNB, který činil 2,6 %.

- Jádrová inflace činí stejně jako v srpnu 2,8 % a je v souladu s odhadem ČNB.

- Bezpečně se nachází v tolerančním pásmu ČNB, které činí 1-3 %.

- Ceny zboží se meziročně zvýšily o 0,8 % (v srpnu 1,1 %) a ceny služeb, které i nadále zůstávají tahounem inflace, vzrostly stejně jako v srpnu o 4,7 %.

- Zářijová meziměsíční inflace činí záporných 0,6 %.

- Harmonizovaný index spotřebitelských cen dle metodiky Eurostatu (HICP) se ze srpnových 2,4 % snížil na 2,0 %, což je pod inflací eurozóny 2,2 %. Je tak názorně vidět, že zůstává nižší než inflace spočítaná dle metodiky ČSÚ.

Struktura míry inflace

- Bydlení: elektřina klesla o 3,5 % (srpnu o 4,1 %), plyn klesá o 8,5 % (v srpnu pokles o 8,0 %), vodné je od ledna meziročně na hodnotě +4,2 %, růst ceny stočného se od ledna také udržuje na +3,7 %.

- Nájemné: +5,7 % (v srpnu +5,7 %), imputované nájemné stejně jako v předcházejících 3 měsících 4,9 %.

- Potraviny alkohol a tabák: 2,9 % (v srpnu +4,0 %); vybrané potraviny, které pomohly zpomalení míry inflace: ceny másla + 5,2 % (v srpnu +11,3 %),

- Stravovací služby: +4,5 % (v srpnu +4,6 %), ubytovací služby stejně jako v srpnu +6,6 %

Míra inflace i nadále zůstává pod odhadem ČNB, její pohled vyjádřený Petrem Sklenářem, ředitelem sekce měnové na vývoj je jasný:

„Ve zbytku roku očekáváme, že míra inflace zůstane poblíž posledních hodnot. Vzhledem ke stále zvýšené jádrové inflaci zůstávají důvody pro opatrnost v měnové politice.“

„Vývoj jádrové inflace ukazuje, že celkový cenový vývoj v domácí ekonomice ještě není plně stabilizován a vyžaduje přísné měnové podmínky.“

Druhý citát ohledně jádrové inflace je identický s komentářem ČNB k inflaci za srpen 2025.

Měla by ČNB zůstat jestřábem? Je čas na uvolnění měnových politik

Rizika vysokých sazeb a přínosy uvolnění

Dlouhodobé udržování vysokých sazeb brzdí investice a spotřebu, zvyšuje nezaměstnanost a zhoršuje dostupnost bydlení i obsluhu dluhu. Opatrné snížení sazeb by naopak podpořilo důvěru investorů a spotřebitelů, zmírnilo finanční tlak na domácnosti, firmy i stát a předešlo hlubšímu propadu. Historické zkušenosti potvrzují, že včasné uvolnění měnové politiky v období stabilní inflace a slabého růstu je efektivní a přispívá k udržitelnému oživení ekonomiky.

ECB: Mírně záporné reálné sazby, přísné podmínky a slabý růst

Zářijový meziroční „flash“ HICP pro eurozónu činí 2,2 %. ECB drží depozitní sazbu na 2,00 % (hlavní refinanční 2,15 %), což při inflaci 2,2 % znamená mírně zápornou ex-post reálnou sazbu. Reálné finanční podmínky však zůstávají přísné kvůli úvěrovým standardům a slabé poptávce.

K tomu přispívá i minimální růst německé ekonomiky a nejistoty ve Francii, které představují riziko pro celý region. Snížení o 25 bazických bodů by pomohlo zmírnit restrikci bez rizika „přešlápnutí“ a lépe sladilo politiku s reálnými podmínkami, aniž by ohrozilo inflační cíl.

Fed: Reakce na zpomalení a nejistoty

Americký Fed v září snížil úrokovou sazbu o 25 bb na 4,00–4,25 %. To reflektuje zpomalující růst a klesající inflaci. Fed naznačil možnost dalších dvou snížení do konce 2025, s důrazem na opatrnost a kredibilitu cíle. Politický pat ve Washingtonu a vládní shutdown od 1. října 2025 zvyšují nejistotu, což tlačí trhy k očekávání rychlejšího snižování úrokových sazeb.

ČNB: Zbytečně restriktivní nastavení

ČNB udržuje 2T repo sazbu na 3,50 % (diskont 2,50 %, lombard 4,50 %). To při HICP 2,0 % vytváří reálnou sazbu +1,5 p. b. – výrazně restriktivnější než v eurozóně. Bez výrazných inflačních tlaků (potraviny i energie se normalizují, lednové přecenění bude mírnější) je prostor pro snížení o 25 p.b. už na nejbližším či následujícím zasedání a pokračování. Tento krok by zmenšil úrokový rozestup vůči ECB a podpořil ekonomiku bez ztráty inflačního ukotvení.

Zhoršení ekonomiky zemí eurozóny negativně ovlivní i českou ekonomiku. Včasné uvolnění zmírní restrikci, podpoří sentiment a přitom zachová kredibilitu inflačního cíle.

V souhrnu platí, že opatrné a datově podmíněné snížení úrokových sazeb pomůže:

- zmírnit náklady na financování pro domácnosti, firmy i státní sektor,

- podpořit důvěru spotřebitelů a investorů,

- ulevit od přehnaných restrikcí, které mohou brzdit ekonomický růst a investice,

- zároveň ponechat prostor pro flexibilní reakci v případě změn inflačních tlaků.

September 2025: Inflation Continues to Slow, Reaching 2.3%. The CNB Should End Its Hawkish Stance

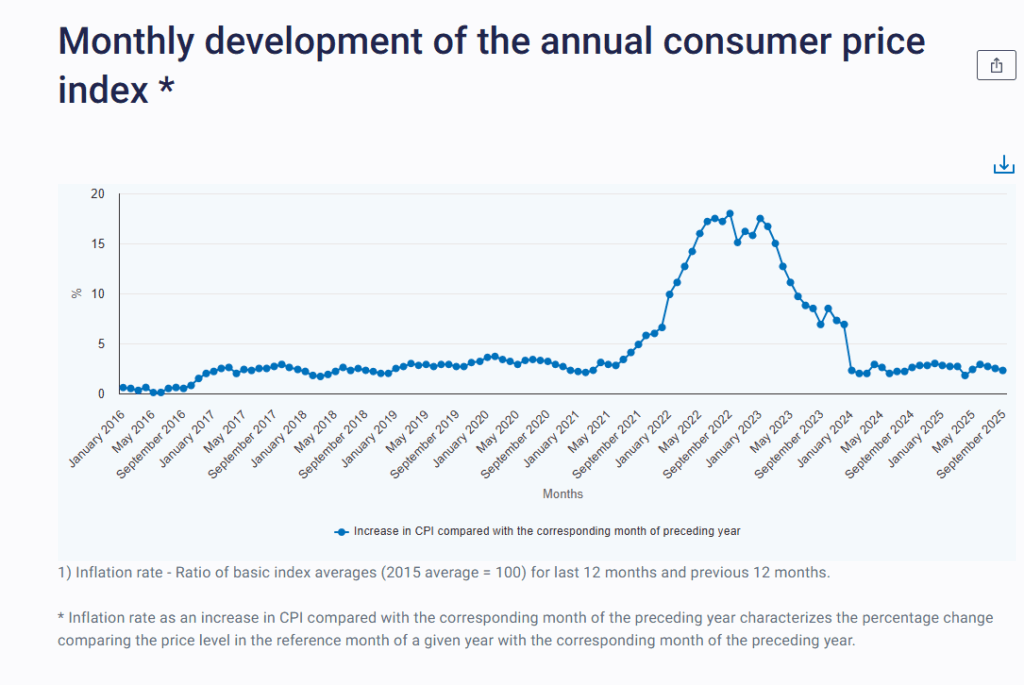

On Friday, October 10, the Czech Statistical Office published the inflation rate for September 2025. As in previous months, the actual figure matched the preliminary estimate released a few days earlier.

- The year-on-year inflation rate continues to ease. The recorded 2.3% is lower than August’s 2.5% and represents the lowest since April.It also undershot the CNB’s 2.6% projection.

- Core inflation remains at 2.8%, unchanged from August and in line with the CNB’s projection.

- Inflation is safely within the CNB’s tolerance band of 1–3%.

- Goods prices increased by 0.8% year-on-year (compared to 1.1% in August), while services prices—still the main driver of inflation—increased by 4.7%, unchanged from August.

- Month-on-month inflation for September was -0.6%.

- The Harmonized Index of Consumer Prices (HICP) according to Eurostat methodology fell from 2.4% in August to 2.0% in September —illustrating that HICP remains lower than the national CPI measured by the CZSO.

Inflation Structure

- Housing: Electricity prices fell by 3.5% (August: −4.1%), gas prices declined by 8.5% (8.0% in August), water prices have been up 4.2% year-on-year since January, and sewage charges have increased by 3.7%, same as from January.

- Rent: Up 5.7% (unchanged from August), with imputed rent at 4.9% unchanged for the third consecutive month

- Food, alcohol, and tobacco: Up 2.9% (August: +4.0%). Selected food items that contributed to the slowdown in inflation include butter +5.2% (August: +11.3%)

- Restaurant services: Up 4.5% (4.6% in August); accommodation services up 6.6%, unchanged from August.

CNB’s view vs. the data

The inflation rate remains below the CNB’s forecast. The CNB’s perspective, as expressed by Petr Sklenář, Executive Director of the Monetary Department, remains cautious:

“We expect inflation to remain close to recent values for the rest of the year. Given the persisting elevated core inflation, there are still reasons for a cautious monetary policy approach.”

“The evolution of core inflation shows that overall price developments in the domestic economy have not yet fully stabilised and require tight monetary conditions”

second statement regarding core inflation is identical to the CNB’s commentary on August 2025 inflation.

Should the CNB Really Remain Hawkish? It Is Time for banks to Ease

Risks of High Rates and Benefits of Easing

Prolonged maintenance of high interest rates suppresses investment and consumption, increases unemployment, and worsens both housing affordability as well as debt servicing costs. Conversely, a cautious rate cut would support investor and consumer confidence, ease financial pressure on households, businesses, and the government, and help prevent a deeper economic downturn. Historical experience confirms that timely monetary easing during periods of stable inflation and weak growth is effective and contributes to a sustainable economic recovery.

ECB: Slightly Negative Real Rates, Tight Conditions, and Weak Growth

September’s preliminary year-on-year HICP for the Eurozone stands at 2.2%. The ECB keeps the deposit rate at 2.00% (main refinancing rate at 2.15%), which, with inflation at 2.2%, results in a slightly negative ex-post real rate. However, overall financial conditions remain tight due to strict credit standards and subdued demand. Added to that are anemic German growth and heightened uncertainty in France, both of which weigh on the regional outlook. A 25 bp cut would reduce unnecessary restraint without “over-steering” and would better align policy with real-economy conditions without jeopardising the inflation target

Fed: Responding to Slowdown and Uncertainty

In September, the Federal Reserve cut the federal funds rate by 25 bp to a range of 4.00–4.25%, reflecting slowing growth and declining inflation. The Fed has indicated the possibility of two further cuts by the end of 2025, emphasizing caution and the credibility of its inflation target. The political gridlock in Washington and the federal government shutdown starting October 1, 2025, have increased uncertainty, and have pushed markets to price faster easing.

CNB: An Unnecessarily Restrictive Stance

The CNB maintains the two-week repo rate at 3.50% (discount rate at 2.50%, Lombard rate at 4.50%). With HICP at 2.0%, results in a real rate of +1.5 percentage points—significantly more restrictive than in the Eurozone. In the absence of significant inflationary pressures (with food and energy prices normalizing and January’s repricing expected to be milder than in recent years), there is room for a 25 basis point cut at the next or subsequent meeting, with further reductions possible. This step would narrow the interest rate gap with the ECB and support the domestic economy without jeopardizing inflation anchoring.

Weakening growth in the euro area will also spill over to the Czech economy. Timely, calibrated easing would soften overall restraint, bolster sentiment, and preserve the credibility of the inflation target.

In sum, a cautious, data-dependent rate reduction would

- Lower financing costs for households, businesses, and the public sector,

- Support consumer and investor confidence,

- Relieve excessive monetary restraint that could hinder economic growth and investment,

- Preserving flexibility to respond to any changes in inflationary pressures.

-

video

video